Annual Disclosure Rituals of US E&P Companies

Annual Disclosure Rituals of US E&P Companies

(Reprinted from an Apr. 2016 article by the author on Seeking Alpha)

January may get off to a slow start for many of us, but E&P companies are busy preparing all sorts of information they will disclose to investors that will summarize their results for 2023 and guide investors on what to expect for 2024. While the years may change, and companies may come and go, the process remains much the same.

So, rather than update info from the 2016 article I published, I am reprinting it in full. As I said, the process has not changed, and the 2023/2024 information will become available any time, offering an opportunity to update prior information then.

Respectful comments are welcome.

Summary

While investors may be hoping for just a bit of holiday cheer, E&P companies embark on a year-end process that will likely be anything but cheerful.

The New Year brings with it many key disclosures, including information about reserves, CAPEX and operational/financial results.

A schedule of typical disclosures and timing is set out and explained so that investors know what to look for and when.

The year 2015 was definitely more knotty than nice to E&P company investors, and as the year winds to a close, many investors are looking for updated information to be provided by the companies they follow. Since I am continually asked, "Where did you get that?" or "When do companies provide that?", I thought it might be useful to describe the process currently underway at all E&P companies for year-end reporting purposes, as well as the expected timing for reporting results from those reviews to investors.

This article is more along the lines of the old saying: "Teach a man to fish... and he'll spend all day in a boat in the middle of a lake drinking beer"... or something like that.

There are several different types of information that get reported to investors at various times throughout each year, but I will focus on the following:

CAPEX

Reserves

Operational/Financial results

Guidance

SEC filings

Banking

Presentations

Material events

CAPEX

Readers may have noticed that some companies have already begun reporting their expected CAPEX plans for next year. With prices changing so drastically, many already cut them during the year, but in most years, an E&P company will set its CAPEX budget in connection with the yearly reserves and planning cycle they do at the end of the year. Most companies will issue a formal press release by early January that details both the total and possibly a breakdown of CAPEX spending by project area.

I will use Range Resources' (RRC) materials for examples throughout this article, since they do an excellent job in conveying necessary information to investors. A typical CAPEX announcement will look like this.

Reserves

A revised summary of reserves as of year-end will typically be issued fairly close in time to the CAPEX estimates, typically by mid- to late-January. This goes into detail to explain changes in SEC values from the prior year-end, costs incurred during the year and the finding costs attributable to reserves added, and how much of production was replaced by reserve additions during the year. A breakdown in changes to SEC values which arose from price changes, expense changes, development, acquisitions/dispositions and technical reserve evaluation is often provided. An example from Range's website can be found here.

Prices to be used for 2015 year-end reserves have already been set because they are based on the 12-month trailing average of prices on the first of each month. December 1, 2015 prices were the last ones necessary, and as a result, companies will show $50.28/bbl for oil and $2.63/mcf for gas, adjusted as necessary to account for regional prices, transportation and other charges back to each individual well.

Readers may not be familiar with reserve disclosures, so Range's 2014 disclosures are presented in the tables below, each of which serves a slightly different purpose.

In the SEC case, future cash inflows are simply the production volumes set out in the reserve report, calculated at the well level and then aggregated for all properties a company owns, then times the price calculated from the year-end price deck, again adjusted back to the well level. Production/LOE costs are per well estimates based on recent actual results, and development costs are estimated costs to be incurred in the future. SEC regs now require an expectation that proved undeveloped (PUD) reserves will be developed within 5 years; otherwise they will not be included.

From the result, future (undiscounted) net cash flows before tax, income taxes based on expected statutory rates are calculated, and a 10% discount factor is applied to determine the present value of the cash flow stream, discounted at 10%. In RRC's 2014 case (based on assumptions of $94 oil and $4.35 natural gas), its SEC value was $7.593 bln.

The changes in SEC10 values from year to year are then computed for various factors, the most important of which are production, price changes and changes due to development, acquisition and disposition of reserves. This helps analysts and investors determine how a company's value changed during the past year due to factors that are often most important to them, and sets the stage for determining how effective a company was in allocating its CAPEX.

The following table summarizes changes in the standardized measure of discounted future net cash flows.

During 2014, the biggest changes were due to current year production ($1.4 bln), more than offset by additions due to purchases and development, less sales ($2.75 bln). So, in 2014, RRC almost replaced the value of what it produced by almost 2:1. But that still doesn't say how big the reserve increase was (as opposed to value) or how efficient RRC was in CAPEX.

The table below summarizes changes to reserves themselves. Net reserve additions were approximately 2.4 TCF against production of 0.4 BCF. Industry disclosures would say that RRC replaced 600% of production during the year, seemingly a good statistic. At year-end, the percent of RRC's reserves which were still classified as undeveloped was almost 50%, indicating both a large program of development going forward and the need for additional CAPEX to do so.

Natural gas at 6.9 TCF out of 10.3 TCF constituted 67% of total reserves. Over 500,000 barrels of ngls computes to 3.0 TCF (at a 6:1 equivalency ratio), or 29%. Oil reserves made up the remaining 4% of reserves.

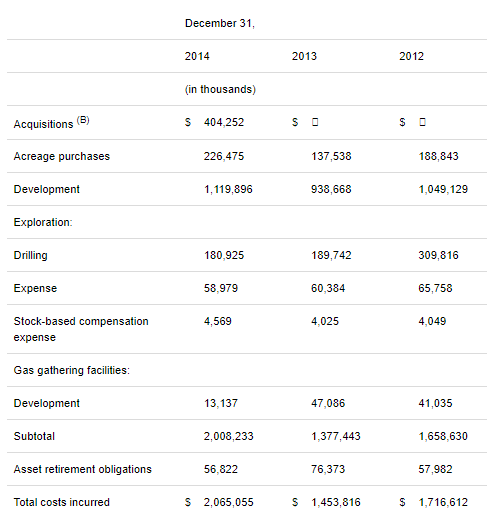

The missing piece of the puzzle is set out in the "Costs Incurred" section, which shows how CAPEX was invested. Without trying to get too detailed, RRC spent roughly $2 bln to add the 2.4 TCF in reserves. This calculates out to a finding cost of $1.20/mcf, and a value replacement of 1.4:1 ($2.75 bln in reserve adds/$2.0 bln in capital). At the time, with year-end prices at $4.35/mcf, those numbers looked very good.

Costs Incurred for Property Acquisition, Exploration and Development

Estimating a year-end 2015 SEC value for RRC would be difficult, since they have continued to be active in drilling and have conducted some sales. Prices alone will take a huge hit, as you might expect with wellhead prices in the Marcellus/Utica where they operate well below the $2.63/mcf base figure. That's why this year's results will be analyzed in great detail and folded into analysts' models and projections as soon as they are released. They will not wait for 10-Ks to be filed to do so.

Operational/Financial Results

By late February, companies will report operational results and summary financial information, both for the 4th quarter of the prior year and for the full calendar year. The financial information will include typical production, revenue, expense, capital and liquidity discussions, possibly with hedging updates where appropriate. Operational discussions will focus on key projects, both for analysis of previous years' activity as well as plans for the upcoming year. Preliminary guidance may also be given, sometimes for the first time, since the focus up to that point will have been on the prior year and companies can be loath to project any further than that.

Range's release dated 2/24/15 is provided here.

SEC Filings

Annual 10-K reports are due by April 15 of each year, but may be filed any time prior to that date. Subsequent quarterly filings are due within 45 days after the end of each quarter. These go into quite a bit more detail on all aspects of a company's business than the summary press releases do, and include full financial statements and notes, data regarding a company's debt, reserves, hedging and other factors.

SEC filings are usually available at company websites. Another, possibly more convenient site is sec.gov, where all filings are available. Range's 10-K was filed in conjunction with its press release on Feb. 24, here.

Banking

Most E&P companies undergo semi-annual bank credit reviews, typically in April and November. The results of those reviews, which result in disclosure of their borrowing bases, are typically the subject of a separate press release given their importance. Some companies may disclose the results in a quarterly press release that summarizes other items as well.

Range's April 2015 review was actually completed and communicated in March, as described here.

Presentations

E&P companies maintain current presentation materials throughout the year that they use to communicate to investors and analysts. These are all available through the respective company's website, with the initial presentation in each year typically the one that carries through most of the year. That initial presentation may appear any time after Jan. 1, but usually in no event later than March. In March and April, the presentation "season" begins, where companies begin to attend conferences with other companies as well to present their "story" to analysts. Important conferences during the year are the IPAA Oil and Gas Investment Symposium (NYC) and the Howard Weil/Scotia Conference in the spring, the Enercom conference in the summer and the IPAA OGIS Conference (SF) in the fall. Companies may also present at smaller conferences hosted by investment firms that provide service to that company.

A list of Range's presentations is here. The main presentations are designated with a date (i.e. Company Presentation December 1, 2015), with investment firm presentations identical to the most recent general one.

Material Events

A good place to look for filings that include more detail than is provided in a press release is at the SEC site. Range's filings are summarized here.

Annual/10-K and quarterly/10-Q statements will be easy to identify, but the search can be limited to just those statements by typing "10" into "Filing type." Alternatively, from the main SEC site, for any company simply type its ticker symbol into "Fast Search" and items should be displayed.

More difficult, but sometimes more interesting, are 8-K filings, which can be used to report anything a company deems material like changes in presentation material, financings, bank updates, transactions, webcasts, etc. Those can be located by typing "8" into the "Filing type." Once you have done it, the process makes it easy to check on companies.

Conclusion

In 2015 especially, it may seem that the Grinch is in complete control of the E&P industry. Whether that is true or not, what is true is that lots of information is available to investors/readers about public companies, and that knowing where and when to look can help avoid companies that might turn worthwhile presents into lumps of coal. Hopefully, reading this brief synopsis will help.