E&P Oil Hedges 2024: Clipped Again

Looks like another year of reduced oil prices along with reduced hedging activity by most E&P companies for 2024. Of course, many companies used higher recent prices to reduce debt, thus reducing risk in that respect. Is the risk of lower oil prices essentially gone given already “lower” prices? Or is hedging something that should be applied consistently in some strategic fashion, much like insuring a home?

As in 2023, the majors are not hedging oil prices, relying on their size and fortress balance sheets to protect them from price drops. In addition, large independents like $APA, $COP, $EOG, $HES, $MGY, $MRO, $MUR, $OXY. Several other companies have been or are in the process of being absorbed into larger companies ($PXD, etc.). Presumably, the acquiring company will implement their own hedging strategy on the combined entity going forward. Lots of Pro Formas to watch out for!

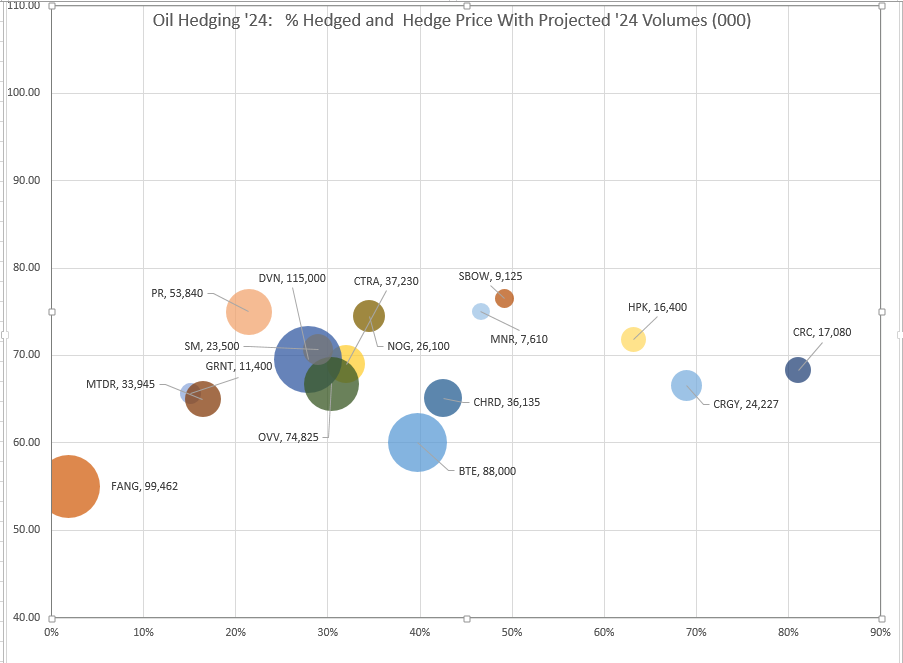

Also as in 2023, the percentage of oil production hedged has declined. Of the companies in the accompanying chart, less than 25% of oil production has been hedged, typically the amount that gets hedged 2-3 years out. So, it appears that companies are more comfortable with more downside exposure with lower current prices. Hedges for 2025 are fewer still, although they would typically be put on as the year progresses.

There has been a fairly significant shift up in the floor prices for oil hedges as well. Downside hedges in the chart show up in the ~$70/bbl range, a pretty significant bump from floors in recent years. Of course, with few hedges in place, the $ downside does not have the same protection that hedges did in prior years.

$FANG remains an outlier in strategy when it comes to hedging, electing to forgo, for the most part, the costless collars employed by most companies. They have purchased a large amount of puts at much lower prices (i.e $55) to protect from disastrous declines in oil prices in 2024. While most companies implement costless collars, which limit upside price participation, $FANG retains that upside. Most collar ceilings are in the $85-$95/bbl range, something I will evaluate if prices move up much more; for now, the downside protection is more the feature I was interested in.

A final note is that obviously the chart below represents a significant amount of production. However, the majors and companies that are consolidating represent a much larger and more financially healthy set of companies, so relying on hedged companies for performance this year may be less impactful than what unhedged companies decide to do.

The chart above includes oil production only, not other liquids. Basis adjustments are not included, nor are ceiling hedge prices. The data was compiled by me from company guidance and presentations, but readers should do their own due diligence. Finally, several companies in the midst of mergers are excluded until new guidance is issued. Small companies and/or companies with relatively small oil production are also excluded.

TY for the update sir!